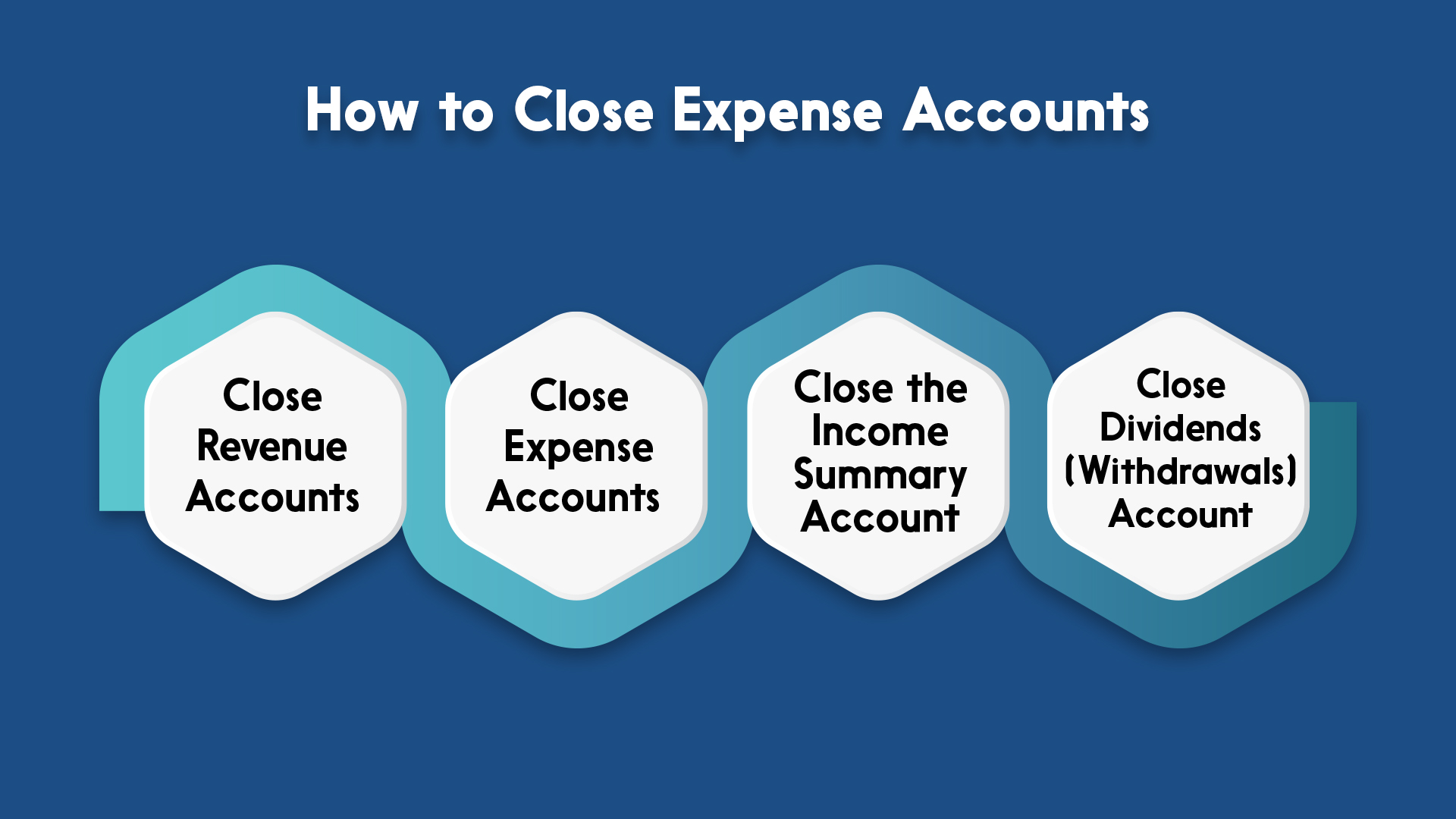

How to Close Expense Accounts: A Simple Process

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the